Annual highlights of the telecommunications sector 2020

© Her Majesty the Queen in Right of Canada, as represented by the Canadian Radio-television and Telecommunications Commission, 2020

ISSN 2564-369X

Catalogue No. BC9-34E-PDF

This report contains highlights of the telecommunications sector for calendar year 2020.

On this page

- Executive summary

- Market composition

- Revenues

- Financial performance

- Sector summaries

- Datasets available on Open Data

- Methodology

i. Executive summary

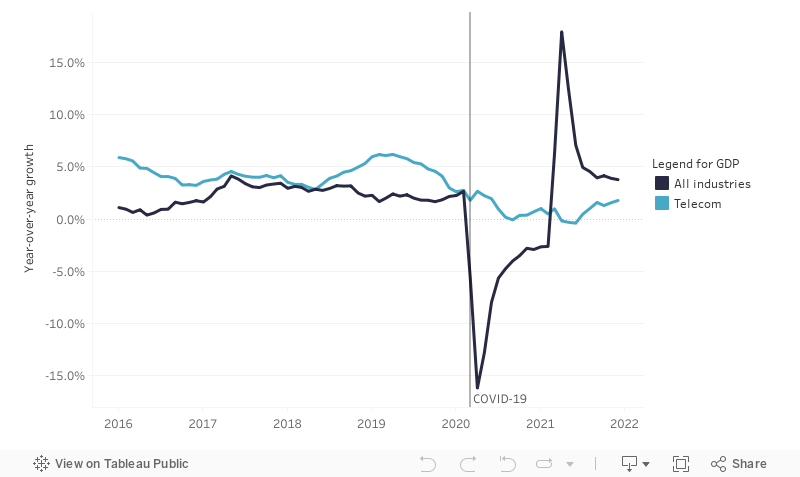

The year 2020 was marked by the COVID-19 pandemic and telecommunications became more important than ever. As non-essential travel was curtailed and many Canadians worked from home, the telecommunications industry recorded higher volumes of wireline voice calling, an exceptional surge in Internet data usage and a decreases in mobile roaming. The telecommunications sectors contribution to GDP slowed in 2020 but fared better in contrast to the economy as a whole, which declined sharply before starting to recover (see Figure 1).

Accessibility

Visual data browsing cannot be done through the screenreader but the equivalent of that graphed data can be downloaded for browsing.

Please note not all of the items listed on the following page apply to our dashboards: Keyboard Accessibility for Tableau on the Web (opens a new window to an external link)

Figure 1 - Gross domestic product (GDP) growth rate (%) in Canada

The telecommunications sector experienced a 1.4% decrease in total revenues in 2020 when compared to 2019, the largest revenue decrease since the CRTC has been publishing the Communications Market Reports (CMR, formerly referred to as the Communications Monitoring Report) (see Figure 2). The only other decrease was recorded in 2002 at the end of the dot-com bubble, which resulted in a less significant 0.3% revenue drop. The decrease in total Canadian telecommunications revenues in 2020 is primarily due to the almost $1B drop in mobile revenues, as total mobile declined 3.3%, decreasing for the first time since the CRTC has been publishing the CMR.

Despite the decline in revenues, wireless carriers, as a group, reported slightly higher EBITDA margin, lower churn rates, and increased capital investments on 5G networks. From the consumer perspective, the average subscriber used more data than ever before and subscribers continued to subscribe to larger data plans.

The retail fixed Internet sector performed relatively well compared to other telecom sectors, growing 4.3% to 14.1 billion of dollars. Continued residential subscriber movement towards higher speed packages drove this growth despite business Internet revenues being impacted by business closures during the pandemic. In addition, with the ongoing pandemic, Internet service is a necessity for Canadians for remote work and education, access news and information, as well as for entertainment. This was evident as data usage surged substantially while many schools and workplaces transitioned online. It was also evident from significant increase in capital investments from fixed wireless service providers who worked to expand access to the Internet.

Lastly, telecommunications service providers recorded an increase in call volumes (partially offset by a lower ARPU) which led to a 0.2% decline in retail long distance revenues in 2020 in a sector that has experienced recent annual declines of about 7%.

Scroll

View data

ii. Market composition

Canadian telecommunications revenues totalled $53.4 billion in 2020, as Canadians used ever-increasing amounts of data through both fixed Internet and mobile services. (“Data usage” includes the use of data for video streaming services such as Netflix and YouTube, as well as for audio streaming services such as Spotify and various radio applications via mobile devices or fixed Internet services.)

Long description

| Sector | 2019 | 2020 | Growth (%) 2019-2020 | CAGR (%) 2016-2020 |

|---|---|---|---|---|

| Mobile | $28.9 B | $27.9 B | -3.3 | 3.4 |

| Fixed Internet | $13.5 B | $14.1 B | 4.3 | 7.0 |

| Local and access | $6.1 B | $5.9 B | -4.3 | -5.1 |

| Data | $3.2 B | $3.1 B | -0.6 | -0.5 |

| Long distance | $1.3 B | $1.3 B | 0.6 | -6.8 |

| Private line | $1.2 B | $1.1 B | -10.9 | -5.2 |

| Total | $54.2 B | $53.4 B | -1.4 | 2.3 |

Total telecommunications revenues is calculated from exact amounts and may appear to differ from total sector revenues due to rounding.

Data may change from year to year for a number of reasons, including economic growth or decline, merger and acquisition activity, industry reclassification, changes in methodology, and revisions to the data.

Service providers are divided into two broad categories: incumbent telecommunications service providers (incumbent TSPs), which provided local telecommunications services on a monopoly basis prior to the introduction of competition, and alternative service providers, which encompass all other types of entities.

Alternative service providers include cable-based carriers, which are the former cable monopolies that currently also provide telecommunications services; other facilities-based service providers; and wholesale-based service providers, which are companies providing services primarily using other companies’ facilities.

Incumbent TSPs, along with cable-based carriers, own and operate the majority of the infrastructure used by other service providers.

Refer to the methodology section for more details.

| Type of TSP | Revenue share (%) | Growth (%) 2019-2020 | CAGR (%) 2016-2020 |

|---|---|---|---|

| Large incumbent TSPs | 56.7 | -1.5 | 1.4 |

| Cable-based carriers | 35.1 | -1.8 | 3.8 |

| Other facilities-based carriers | 3.7 | 9.3 | 4.0 |

| Wholesale-based service providers | 3.5 | -8.4 | 1.9 |

| Small incumbent TSPs | 1.0 | 2.8 | 2.4 |

Source: CRTC data collection

Examples of large incumbent TSPs include Bell, SaskTel, and TELUS.

Examples of small incumbent TSPs include Execulink and Sogetel.

Examples of cable-based carriers include Rogers, Shaw, and Vidéotron.

Examples of other facilities-based carriers TSPs include Allstream Business and Xplornet.

Examples of wholesale-based service providers include Distributel and TekSavvy.

Growth and CAGR are calculated from the revenues in billions of dollars.

The five largest providers of telecommunications services (including affiliates) accounted for 86.9% of total revenues in 2020. These company groups are Bell, Rogers, Telus, Shaw, and Quebecor. They are a mix of incumbent TSPs and cable-based carriers, and all are facilities-based service providers. The percentage of revenues represented by the top five changes slightly from year to year. Significant changes are usually due to factors such as ownership transfers.

Generally, since 2016, the share of large and small incumbent TSPs’ revenues has been declining by about one or two percentage points per year on average. During the same period, the revenue market share of cable-carriers increased by approximately two percentage points to 35.1% in 2020.

While large incumbent TSPs represented 0.6% of all telecommunications providersFootnote 1 in 2020, they generated 56.7% of revenues. Cable-based carriers made up 7.1% of the total number of telecommunication providers and generated 35.1% of revenues. With relatively lower barriers to entry, wholesale-based service providers comprised nearly 66.5% of service providers while generating 3.5% of revenues.

Scroll

View data

Source: CRTC data collection

Scroll

View data

Source: CRTC data collection

iii. Revenues

In the Communications Market Report, telecommunications services are divided into six sectors:

Long description

| Type | Subtype | Sector | 2020 |

|---|---|---|---|

| Wireline | Wireline voice | Local and access | 11.0% |

| Wireline | Wireline voice | Long distance | 2.5% |

| Wireline | Wireline data | Data | 5.9% |

| Wireline | Wireline data | Private line | 2.0% |

| Wireline | Wireline data | Fixed Internet | 26.4% |

| Wireless | Mobile voice and data | Mobile | 52.3% |

In 2020, nine company groupingsFootnote 2 offered services in all six telecommunications sectors, accounting for 85.7% of total telecommunications revenues in Canada. These large, facilities-based entities tend to offer a wider array of services than their smaller counterparts. At the other end, companies providing services from one to three service sectors generally offered Internet access, local phone service, or long-distance phone services. These smaller entities, often wholesale-based service providers, represented 72% of all TSPs and generated 4.7% of telecommunications revenues in 2020.

Scroll

View data

Scroll

View data

The six service categories include: Local and access, Long distance, Data, Private line, Internet and Mobile.

Retail versus wholesale

Telecommunications services revenues come from both retail sales (i.e., sales to residential consumers and business customer) and wholesale sales (i.e., sales to other providers of telecommunications services).

Long description

| Description of service | Type of TSP | Market | Category | 2019 | 2020 |

|---|---|---|---|---|---|

| Services provided directly to the end-user | Retail services are generally provided by all TSPs |

Retail | Revenue share | 92.5% | 92.3% |

| Services provided directly to the end-user | Retail services are generally provided by all TSPs |

Retail | Revenues | $50.2 B | $49.3 B |

| Services provided by one TSP to another, then to the end-user |

Wholesale services are provided by facilities-based TSPs |

Wholesale | Revenue share | 7.5% | 7.7% |

| Services provided by one TSP to another, then to the end-user |

Wholesale services are provided by facilities-based TSPs |

Wholesale | Revenues | $4.1 B | $4.1 B |

Retail revenues decreased slightly to account for 92.3% of total telecommunications revenues in 2020, hovering around 92% to 93% over the past five years. 95.8% of mobile revenues were generated from retail services, compared to 88.5% for wireline. Those numbers have remained virtually unchanged since 2013.

Retail and wholesale mobile roamingFootnote 3 revenues were severely impacted by COVID-19. The retail mobile roaming and other revenues represented approximately 4% of total retail mobile revenues in 2019 compared to approximately 3% of in 2020. Total wholesale mobile roaming revenues dropped by approximately 13% in 2020. Roaming revenues were largely generated from subscribers who used mobile services in the United States. Short Message Service (SMS) and Multimedia Messaging Service (MMS) revenues were excluded from the data revenue component of this figure.

Canadian retail telecommunications service revenues decreased 1.7% to $49.3 billion in 2020. In Ontario, these services had the largest share (36.2% or $19.4 billion) of all telecommunication revenues amongst the provinces and territories. Quebec had the second largest retail revenue share at 18.6% ($9.9 billion), followed by British Columbia at 12.4% ($6.6 billion) and Alberta at 11.9% ($6.3 billion).

The wholesale telecommunications market saw a similar trend, with Ontario leading the provinces/territories at 3.6% ($1.9 billion) of all telecommunication revenues, followed by Quebec at 1.7% ($0.9 billion) and the prairies region with 1.0% ($0.5 billion).

Scroll

View data

Source: CRTC data collection

The number of wholesale Internet lines increased in 2020, growing by 0.1% to over 1.3 million lines across Canada. Ontario maintained the highest share of wholesale lines with 0.8 million lines (59.4%); Quebec trailed behind with 0.4 million (27.4%), and the rest of Canada totaled approximately 0.2 million (13.3%).

The Atlantic region (Newfoundland and Labrador, New Brunswick, Prince Edward Island, and Nova Scotia) saw significant growth in the number of wholesale lines, growing from approximately 37,000 to 47,000 lines (26.1%). This increase can be largely attributed to the continued growth in Nova Scotia, which added over 7,000 wholesale lines in 2020.

Scroll

View data

Source: CRTC data collection

Information in this figure regarding Internet wholesale lines is from the larger ISPs. They reported approximately 98% of total Internet wholesale lines in 2020.

Forborne services

Over time, the Commission has refrained from regulation when it finds that a service is subject to sufficient competition or where refraining from regulation is consistent with the Canadian telecommunications policy objectives, as outlined in section 7 of the Telecommunications Act. This is referred to as forbearance. Where a service is forborne from regulation, the provider is generally relieved of the obligation to provide the service pursuant to a Commission-approved tariff. The Commission generally does not regulate retail rates.

| Sector | 2016 | 2017 | 2018 | 2019 | 2020 |

|---|---|---|---|---|---|

| Local and access | 82.0 | 83.0 | 83.0 | 83.6 | 83.1 |

| Long distance | 98.2 | 98.4 | 98.4 | 98.6 | 98.7 |

| Data | 95.9 | 96.0 | 96.0 | 96.0 | 96.0 |

| Private line | 71.6 | 71.9 | 71.9 | 75.5 | 74.1 |

| Internet | 96.7 | 97.2 | 97.2 | 97.0 | 96.4 |

| Mobile | 99.9 | 99.8 | 99.8 | 99.8 | 99.8 |

| Overall | 95.4 | 95.6 | 95.6 | 96.5 | 96.3 |

Source: CRTC data collection

In 2020, approximately 96.3% of telecommunications revenues have been generated from forborne services. The percentage of revenues derived from forborne services ranged from a low of 74.1% in private line, to a high of 99.8% in mobile.

Canadian ownership

Section 16 of the Telecommunications Act addresses the eligibility of Canadian companies to operate as telecommunications common carriers.

Subject to certain exceptions, section 16 requires that telecommunications companies that own or operate telecommunications transmission equipment and have Canadian telecommunications revenues greater than $5.3 billion (10% of total Canadian telecommunications revenues) be Canadian-owned and controlled.

For the purposes of applying the provisions of section 16, the Commission has determined that total annual revenues from the provision of telecommunications services in Canada was $53.4 billion in 2020.

Contribution – subsidization of high-cost residential local telephone service

The total amount of subsidies paid to local exchange carriers (LECs) was $49.9 million in 2020, down from $71.4 million (30.2% decrease) in 2019.

This subsidy represents revenue contributions toward the provision of residential telephone service in high-cost serving areas (HCSAs) by TSPs, or groups of related TSPs that have a minimum of $10 million in annual Canadian telecommunications revenues. HCSAs are areas where the cost of providing service is substantially higher than in other parts of an incumbent LEC’s territory. HCSAs are often remote or rural areas.

In Telecom Regulatory Policy 2016-496, the Commission stated that in order to help meet the new universal service objective, it would begin to shift the focus of its regulatory frameworks from wireline voice services to broadband Internet access services.

Scroll

View data

Source: CRTC data collection

iv. Financial performance

This section of the highlights of the telecommunications sector focuses on metrics such as capital expenditures made into acquiring spectrum, capital intensity, earnings before interest, taxes, depreciation and amortization (EBITDA). These are key indicators that can be used to evaluate the financial performance of the Canadian telecommunication industry by showing the amount of capital that is being reinvested back into maintaining and improving telecommunications networks. Looking at churn, despite the different lens of retail and business subscriptions, also provides an interesting perspective.

Long description

| Metric | Category | 2016 | 2020 |

|---|---|---|---|

| Capital expenditures ($ billions) | Wireline | $9.2 B | $8.6 B |

| Capital expenditures ($ billions) | Mobile | $2.3 B | $2.8 B |

| Capital intensity (%) | Mobile providers | 9.6% | 10.0% |

| Capital intensity (%) | Wireline incumbents TSPs | 40.4% | 40.9% |

| Capital intensity (%) | Wireline cable-based carriers and other facilities-based carriers | 46.5% | 34.8% |

| EBITDA margin (%) | Wireline | 33.3% | 36.1% |

| EBITDA margin (%) | Mobile | 43.4% | 46.0% |

| Investment in spectrum ($ millions) | Mobile | $150.0 M | $152.8 M |

Capital expenditures and capital intensity

Capital expenditures, or CAPEX, are investments made primarily to maintain or upgrade telecommunications networks. As such, it is a leading indicator for economic and business conditions of the telecommunications industry in Canada. With COVID-19 restrictions and their impacts, many companies had slowed the flow of capital investments. In 2020, total capital expenditures dropped 3.9% with wireline and wireless reporting a 3.5% and 5.0% decline, respectively. Despite the drop in overall wireless expenditures, $480 million was invested for 5G networks which represented approximately 17.7% of the total wireless capital spent in 2020. As COVID-19 restrictions are gradually lifted, we will continue to monitor the overall level of capital expenditures in Canada with a keen eye on 5G capital investments.

Between 2016 and 2020, wireline CAPEX decreased at an average annual rate of 1.8%. The large incumbent TSPs’ share of wireline CAPEX has seen an increase from 59.8% to 63.8% over the same period. The wireline CAPEX share of cable-based carriers has decreased from 38.4% in 2016 to 30.9% in 2020. Telecommunications service providers with over $100 million in revenues spent $11.4 billion on CAPEX, $8.6 billion of which was spent on wireline networks.

Scroll

View data

Source: CRTC data collection

The telecommunications industry is capital intensive, taking considerable investment to build, maintain, and, upgrade extensive network infrastructure. In 2020, the capital intensity of the telecommunications industry was 22.7%, behind the utilities industry, educational services, health care and social assistance industry, and transportation and warehousing industry.

The capital intensity of the Top 5 groups (Bell, Rogers, Shaw, TELUS, and Quebecor) was 22.5%. These TSPs accounted for 90.5% of the total telecommunications CAPEX in 2020, a decrease from 92.6% in 2019.

Scroll

View data

Source: CRTC data collection and Statistics Canada Tables 34-10-0035-01 and 33-10-0226-01

Since many carriers do not recognize and report spectrum as a CAPEX, the investments made in spectrum were not included in the figure above.

Wireline capital intensity (the ratio of capital expenditures to revenues) can fluctuate. It was on the decline for both the incumbent TSPs and cable-based carriers, decreasing from approximately 43.9% in 2016 to 38.4% in 2020. However, capital intensity of wireline other facilities-based service providers increased from 22.4% in 2019 to 42.4% in 2020. This rise was driven by a significant increase in wireline other facilities-based service provider capex to expand and enhance networks.

Wireless capital intensity for mobile providers remained stable. It was around 9.6% in 2016 compared to 10.0% in 2020.

Scroll

View data

Source: CRTC data collection

Earnings before interest, taxes, depreciation and amortization (EBITDA)

EBITDA margins (i.e., EBITDA as a percentage of total telecommunications revenues) are instrumental in assessing the financial performance of a company or group of companies. Margins are calculated for TSPs with at least 80% of their total revenues represented by telecommunications services. For more details about how EBITDA was derived, see the methodology section.

Over the 2016-2020 period, margins for wireless services were consistently above those for wireline, with the difference widening to approximately 9.9% as wireless margins reached 46.0%, in 2020.

Scroll

View data

Source: CRTC data collection

Over the 2016-2020 period, the average EBITDA margins were at around 43.1% for the cable-based carriers and 39.2% for the incumbents.

Investment in spectrum

Annual investments in spectrum from 2014 to 2020 were $5.26 billion (2014), $2.96 billion (2015), $0.15 billion (2016), $0.44 billion (2017), $0.12 billion (2018), $3.5 billion (2019), and $0.15 billion (2020) respectivelyFootnote 4. Investments made from 2014 to 2020 reflect investments made by mobile carriers to acquire Advanced Wireless Services-3 (AWS-3), Personal Communications Services-GSM bands (PCS-G), and 700 megahertz (MHz), 2300 MHz, 2500 MHz, and 600 MHz spectrum.

Churn

The average churn rate is a measure of subscriber turnover. A high churn rate suggests that customers are leaving their existing providers for a number of reasons, including dissatisfaction with the service, pricing issues or a desire to take advantage of competitive offers. Conversely, low churn rates indicate that customers are not switching providers, which may indicate that customers see value in remaining with their current provider or that there are a lack of incentives motivating them to switch providers, including a lack of alternatives. Average monthly mobile churn rates have been steadily decreasing over the past four years, going from 1.5% in 2016 to 1.1% in 2020. Average monthly residential Internet churn rates have decreased from 1.8% in 2019 to 1.6% in 2020. Similarly, average monthly business Internet subscription churn has decreased from 1.3% to 1.2% over the same period.

v. Sector summaries

In 2020, total Canadian telecommunications revenues experienced a negative growth rate for the first time in over a decade, decreasing 1.4% to $53.4 billion. Total retail telecommunications revenues, which represent the vast majority of telecommunications revenues, totaled $49.3 billion in 2020, decreasing 1.7% from 2019 to 2020, and, on average, growing 2.5% annually from 2016 to 2020. The only sector that recorded revenue growth was fixed Internet services which saw a 3.9% increase in 2020.

Long description

| Sector | Mobile | Fixed Internet | Long distance | Data | Local and access | Private line |

|---|---|---|---|---|---|---|

| Retail revenues ($ billions) | $26.8 B | $13.3 B | $1.0 B | $2.3 B | $5.3 B | $0.6 B |

| Retail revenue growth (%) | -3.2% | 3.9% | -0.2% | -4.1% | -5.1% | -10.1% |

In terms of retail revenues, the mobile sector was the main contributor to the overall loss in total retail telecommunications revenues in 2020. For the first time ever, mobile reported a negative growth rate which saw the sector shed approximately $900 million or 3.2% in 2020, but still remained the largest sector, accounting for over half (54.2%) of all retail telecommunications revenues in 2020. The fixed Internet sector made up over a quarter (27.0%) of all retail revenues and was the only sector to grow in revenues over the previous year, increasing 3.9%. Revenues of all remaining sectors continued to decline over the past five years.

Average residential fixed Internet revenue per subscriber increased from $55.43 in 2016 to $62.61 in 2020 as users migrated to higher speeds and plans with more data.

This section will provide a brief summary of the six retail sectors (mobile, fixed Internet, local access, long-distance, data, and private line) and the wholesale market within the Canadian telecommunications industry. Additional data for all markets can be found in Open Data.

Retail mobile sector – A focus on mobile phone

In 2020, CRTC revamped the data collections for the mobile sector to capture mobile services in three distinct categories: 1. Mobile phone 2. Mobile broadband and 3. Other plans for mobile connected devices. This restructure will help to align reporting changes in the industry, provide a clearer and more accurate representation of the various segments, specifically mobile phone services, within the mobile sector and will assist in the monitoring efforts of new and innovative mobile solutions for industrial applications, M2M, etc., delivered on 5G mobile networks and beyond. Due to reporting limitations, some estimates were made when deriving each of the three mobile service categories. Furthermore, some previous metrics cannot be reported in 2020. As a result, many of the 2020 metrics will not be comparable to previous years’ data and therefore, growth and cumulative growth rates will not be applicable and will be identified as “NA”. For a description of the three distinct mobile service categories, see the methodology section.

In addition, there will be limited reporting on aggregate mobile statistics in the retail mobile sector, instead, the focus will be on “Mobile phone” services; this will be identified as “MP” which indicates that only mobile phone statistics were included unless specified otherwise.

Metrics that were reported prior to 2020 will be left unchanged, but the 2020 metrics will be impacted. Many metrics that were closely monitored in previous CMR reports have been modified in 2020, including the methodologies. For example, the average monthly data usage per user reported prior to 2020 will remain as is, but in 2020, this metric has been reclassified and reported as the average monthly data usage per mobile phone (MP) data subscriber. Similarly, the average revenue per user (ARPU) was reclassified as the average revenue per user for mobile phone (ARPU-MP).

| Retail mobile | 2019 | 2020 | 2020 (MP) |

|---|---|---|---|

| Total mobile sector revenues ($ billions) | $27.6 B | $26.8 B | NA |

| Mobile phone revenues ($ billions) | NA | NA | $25.9 B |

| Mobile broadband revenues ($ billions) | NA | $0.4 B | NA |

| Other plans for mobile connected devices revenues ($ billions) | NA | $0.4 B | NA |

| Subscribers (millions) | 34.4 M | NA | 32.4 M |

| Annual revenue growth (%) | 2.0% | -3.2% | NA |

| Revenue CAGR (%) 2016-2020 | 5.3% | 3.6% | NA |

| Subscribers with data plans (%) | 90.0% | NA | 84.6% |

| Average mobile data subscriber monthly data usage (GB) | 2.9 GB/month | NA | 3.7 GB/month |

| Monthly ARPU ($) | $68.17 | NA | $66.70 |

| Blended prepaid/postpaid average churn rate of Canada’s Top 3 mobile service providers (%) |

1.38% | NA | 1.20% |

Source: CRTC data collection

Churn is a measure of the number of customers a service provider loses on a monthly basis relative to that service provider’s total subscriber base. It is calculated by dividing the number of customers who have cancelled their service in a month by the total number of subscribers for that service provider over the same period.

Due to the changes to mobile reporting, for 2020, mobile phone (MP) ARPU was calculated by dividing the whole-year total revenue by the number of subscribers from the current year. The number of subscribers is taken from year end data.

| Component | 2016 | 2017 | 2018 | 2019 | 2020 (MP) | Growth (%) 2019-2020 |

CAGR (%) 2016-2020 |

|---|---|---|---|---|---|---|---|

| Basic voice | 8,834.3 | 9,219.7 | 7,747.3 | 7,718.4 | 7,055.1 | NA | NA |

| Long-distance | 547.0 | 481.9 | 417.4 | 367.5 | 366.3 | NA | NA |

| Paging | 11.1 | 8.9 | 9.0 | 4.2 | 1.7 | NA | NA |

| Terminal equipment (including handheld devices) |

1,911.1 | 1,896.1 | 6,961.9 | 7,121.8 | 6,330.5 | NA | NA |

| Data | 10,980.5 | 11,832.4 | 10,857.0 | 11,284.0 | 11,355.4 | NA | NA |

| Roaming and other | 960.0 | 1,047.2 | 1,125.0 | 1,151.3 | 794.0 | NA | NA |

| Data, roaming, and other – subtotal |

11,940.4 | 12,879.6 | 11,982.0 | 12,435.2 | 12,149.4 | NA | NA |

| Total | 23,243.9 | 24,486.2 | 27,117.7 | 27,647.1 | 25,903.0 | NA | NA |

Source: CRTC data collection

IFRS 15 came into effect on 1 January 2018 for all Canadian publicly accountable enterprises. Under the new accounting standards, revenues are recognized upon control of goods or services, impacting mainly the terminal equipment revenues in 2018.

In 2020, the retail mobile sector was not immune to the negative impacts of COVID-19 which put extensive financial pressures across many industries and sectors within the Canadian economy in 2020. For the first time ever, total retail mobile experienced negative revenue growth. Revenues declined from $27.6 billion in 2019 to $26.8 billion in 2020 or a negative 3.2% growth rate. The decline could be attributed to several key factors such as more people worked from home who may have resorted to alternative voice solutions i.e. home phone service, skype, zoom, MS Teams, etc. and the drop in international roaming revenues as global travel restrictions were imposed and enforced throughout 2020. Also, with the restrictions to retail stores and malls, this had a direct impact on mobile equipment and device sales as store traffic was severely reduced or halted altogether. Despite all these challenges, mobile still remained the largest sector, representing over 54.2% of all retail telecommunications revenues in 2020 and the average subscriber consumed more data than ever; this illustrated the resilience of Canada’s mobile operators and Canadians reliance on mobile communications.

There were 32.4 million mobile phone (MP) subscribers in 2020, with mobile networks covering approximately one-fifth of Canada’s geographic land mass and reaching 99.7% of Canadians. In 2020, advanced wireless networks such as LTE-A, continued to deliver higher speeds than previous generation networks. LTE-A was available to approximately 97.4% of Canadians in 2020, compared to 96.0% in the previous year. In 2020, 5G networks were launched and were available to 53.3% of Canadians; there were a total of four 5G operators who offered 5G services, mostly, in selective urban cities and centres.

Long description

| Retail mobile | 2019 | 2020 |

|---|---|---|

| Canadians with access to LTE (%) | 99.5% | 99.5% |

| Major roads and highways covered by LTE (%) 2019-2020 | 88.8% | 88.5% |

| Canadians with access to LTE-A (%) 2019, 2020 | 96.0% | 97.4% |

| Canadians with access to 5G | NA | 53.3% |

The mobile sector continued to be dominated by the three largest mobile service providers (Top 3), Bell GroupFootnote 5, Rogers, and TELUS. In 2020, these entities accounted for 88.6% of retail mobile phone (MP) revenues. The Top 3 held the majority of mobile phone (MP) revenue share in each province/territory, except in Saskatchewan where the other providers captured 60.7% of the mobile phone (MP) sector.

Scroll

View data

Source: CRTC data collection

Other mobile providers include SaskTel, Freedom Mobile, Vidéotron, and Bragg Communications and wholesale-based service providers.

More data on mobile and other telecommunications services can be found in Open Data and their respective sections of the Communications Market Reports.

Retail fixed Internet sector

Long description

| Retail fixed Internet | 2019 | 2020 |

|---|---|---|

| Retail fixed Internet revenues ($ billions) | $12.8 B | $13.3 B |

| Revenue growth rate (%) | 9.0% | 3.9% |

| Revenue CAGR (%) 2016-2020 | 8.7% | 7.0% |

| Retail fixed Internet subscribers (millions) | 15.2 M | 15.9 M |

| Residential fixed Internet | 2019 | 2020 |

|---|---|---|

| Households with a fixed Internet subscription (%) | 90.7% | 94.6% |

| Households with access to 50/10 Mbps speeds with an Unlimited data option (%) |

87.4% | 89.5%Footnote 6 |

| Average download speed (Mbps) | 176.9 Mbps | 220.4 Mbps |

| Subscribers to 50+ Mbps service (%) | 61.6% | 67.7% |

| Average monthly data usage (GB) | 263.6 GB/month | 385.7 GB/month |

| Monthly ARPU ($) | $61.77 | $62.61 |

| Type | Component | 2016 | 2017 | 2018 | 2019 | 2020 | Growth (%) 2019-2020 |

CAGR (%) 2016-2020 |

|---|---|---|---|---|---|---|---|---|

| Residential | Access | 8,090.5 | 8,804.2 | 9,385.0 | 9,992.9 | 10,562.7 | 5.7 | 6.9 |

| Applications, equipment, and other Internet-related services | 289.5 | 314.1 | 419.6 | 505.5 | 555.6 | 9.9 | 17.7 | |

| Total | 8,380.0 | 9,118.3 | 9,804.6 | 10,498.4 | 11,118.3 | 5.9 | 7.3 | |

| Business | Access and transport | 1,442.0 | 1,501.5 | 1,575.7 | 1,894.0 | 1,838.3 | -2.9 | 6.3 |

| Applications, equipment, and other Internet-related services | 356.5 | 347.2 | 385.1 | 437.6 | 379.6 | -13.3 | 1.6 | |

| Total | 1,798.4 | 1,848.7 | 1,960.8 | 2,331.7 | 2,217.9 | -4.9 | 5.4 | |

| All | Total | 10,178.4 | 10,967.0 | 11,765.4 | 12,830.1 | 13,336.2 | 3.9 | 7.0 |

Source: CRTC data collection

Fixed Internet service continue to be an important service. This has been especially evident during the COVID-19 pandemic where Canadians relied on their Internet service for remote work and education, access news and information, as well as for entertainment. This was evident as data usage surged substantially while many schools and workplaces transitioned online. Canada’s broadband networks showed resiliency and flexibility in managing increased demand and maintaining service throughout this challenging and unprecedented period.

The retail fixed Internet sector was the only retail telecommunications sector to experience revenue growth in 2020, growing 3.9% to $13.3 billion. This growth is mainly attributed to the increase in residential Internet access revenues which grew from $10.0 billion in 2019 to $10.6 billion in 2020 (or 5.7% growth). Residential Internet revenues increased as households increasingly subscribed to Internet packages with faster speeds and higher usage limits.

Business Internet revenues were impacted by closures of small-medium sized businesses during the pandemic. This caused total business fixed Internet revenues to experience a negative growth rate for the first time in the past ten years, decreasing from $2.3 billion in 2019 to $2.2 billion in 2020 (or -4.9% growth).

The number of residential subscribers continued to grow, reaching approximately 14.4 million subscriptions (or 94.6% of Canadian households) in 2020, a 4.8% increase from 2019 and more than eight times the population growth rate (0.6%). Cable-based carriers and incumbent TSPs accounted for the majority of subscribers (85.2%), while other entities accounted for 14.8%, up from 12.6% in 2016.

Migration towards higher speed Internet packages continued as the needs of Canadians changed during the pandemic and expanded deployment of fibre and enhanced fixed wireless technologies improved accessibility to these types of packages. The proportion of residential subscriptions to services offering speeds of 100 Mbps or faster grew from 41.7% in 2019 to 47.8% in 2020. 8.3% of subscriptions were for services offering speeds of at least a gigabit in 2020 compared to 5.6% in 2019.

In 2020, there was an abnormal growth in data consumption as Canadians are spending more time online for school, work, and play. The average amount of data downloaded by residential Internet subscribers increased by more than 100GB/month over the past year, from 243.9 GB per month in 2019 to 353.4GB per month in 2020 (44.9% growth). The average upload amounts also grew considerably, from 19.6 GB/month to 32.4 GB/month over the same period (or 64.9% growth). Increased adoption of video teleconferencing services and large file sharing may have contributed to this growth in upload usage.

Retail wireline voice sector

| 2019 | 2020 | |

|---|---|---|

| Retail wireline voice revenues | $6.5 B | $6.2 B |

| Retail wireline voice subscribers | 13.6 M | 13.3 M |

| Revenue growth rate | -8.0% | -4.1% |

| Revenue CAGR (5 year) | -6.7% | -5.6% |

Source: CRTC data collection

| Service | 2016 | 2017 | 2018 | 2019 | 2020 | Growth (%) 2019-2020 |

CAGR (%) 2016-2020 |

|---|---|---|---|---|---|---|---|

| Gross local revenues | 6,635 | 6,474 | 6,086 | 5,584 | 5,296 | -5.2 | -5.5 |

| Less: contribution revenues | 105 | 98 | 87 | 71 | 50 | -30.2 | -17.1 |

| Retail local revenues | 6,529 | 6,376 | 5,999 | 5,513 | 5,246 | -4.8 | -5.3 |

| Retail long distance revenues | 1,287 | 1,095 | 1,052 | 970 | 968 | -0.2 | -6.9 |

| Total local and long distance retail revenues | 7,817 | 7,471 | 7,051 | 6,483 | 6,214 | -4.1 | -5.6 |

Source: CRTC data collection

In 2020, the retail wireline voice sector reported $6.2 billion in revenues, with a 5.6% average annual decline since 2016. Local revenues (excluding contributions) accounted for 84.0% of retail wireline voice revenues in 2020. Long-distance revenues were approximately $968 million, declining by an average annual rate of 6.9% since 2016.

Increased call volumes related to COVID-19 led to a flattening of long distance revenues in 2020, as compared to recent annual declines of about 10%. COVID-related impacts could be seen in increased voice and video call volumes and additional demand for teleconference bridges and 1-800 numbers.

From 2016 to 2020, residential wireline voice revenues per line decreased by $3.94 to $31.37 per month, while business revenues decreased by $3.89 to $51.07 per month. This is, however, a slight increase from 2019 when business revenues were $50.45.

The incumbent carriers accounted for 66.4% of the residential sector of retail wireline revenues, essentially unchanged from 2019, and 76.1% of the business sector, a 1.1% decrease since 2019. Residential revenue shares for facilities-based non-incumbent service providers represented 27.1% of residential retail wireline revenues, in 2020.

Introduction of access-independent VoIP servicesFootnote 7 has opened the wireline voice sector to non-traditional providers. There were approximately 850,000 subscribers to access-independent VoIP in 2020, representing 17% of retail VoIP. This percentage has increased over the last several years with the introduction of new participants.

There were 28,000 payphones in 2020, generating an average of $311 in annual revenues per unit, compared to 58,000 payphones generating $385 per unit in 2016. The number of payphones dropped by over 3,000 or 10.8% from 2019 to 2020, while the average revenue per phone decreased by $63 or 16.8%.

Retail data and private line sector

| 2019 | 2020 | |

|---|---|---|

| Retail data and private line revenues | $3.1 B | $3.0 B |

| Revenue growth rate | -3.2% | -5.4% |

| Revenue CAGR (5 year) | -2.4% | -2.9% |

Source: CRTC data collection

| Sector | Subsector | 2016 | 2017 | 2018 | 2019 | 2020 | Growth (%) 2019-2020 |

CAGR (%) 2016-2020 |

|---|---|---|---|---|---|---|---|---|

| Data | Data protocols | 1,870 | 1,864 | 1,845 | 1,739 | 1,691 | -2.8 | -2.5 |

| Other | 731 | 694 | 690 | 698 | 647 | -7.3 | -3.0 | |

| Total | 2,600 | 2,558 | 2,535 | 2,436 | 2,338 | -4.1 | -2.6 | |

| Private line | Total | 738 | 721 | 700 | 695 | 624 | -10.1 | -4.1 |

| Total | Total | 3,339 | 3,279 | 3,235 | 3,131 | 2,962 | -5.4 | -2.9 |

Source: CRTC data collection

Data and private line services refers to services sold by TSPs to business customers for the transmission of data, video and voice traffic. These services provide private and highly secure communications channels between locations. Data and private line revenues have been in decline since 2014.

Data services are packet-based services that intelligently switch data through carrier networks. They make use of newer data protocols such as Ethernet and Internet Protocol (IP), or legacy data protocols such as X.25, asynchronous transfer mode (ATM), and frame relay to transmit data. Legacy services make up less than 0.4% of revenues. The subcategory “Other” includes network management and networking equipment.

Private line services provide non-switched, dedicated communications connections between two or more points to transport data, video and/or voice traffic.

Data posted a 4.1% loss in 2020, on par with 2019, but a higher loss than the 2016-2020 average of 2.6%.

Private line with a 10% loss in 2020 exceeded the 2016-2020 average decline of 4.1%.

Incumbent TSPs accounted for approximately 65.5% of retail data revenues and 61.0% of retail private line revenues in 2020, compared to 64.2% and 74.3% for data and private line in 2016.

Wholesale

| 2018 | 2019 | 2020 | |

|---|---|---|---|

| Wholesale revenues | $3.844 B | $4.053 B | $4.115 B |

| Revenue growth rate | -4.4% | 5.4% | 1.5% |

| Revenue CAGR (5 year) | 0.4% | 0.8% | 0.4% |

Source: CRTC data collection

| Type | Sub-type | Sector | 2016 | 2017 | 2018 | 2019 | 2020 | Growth (%) 2019-2020 |

CAGR (%) 2016-2020 |

|---|---|---|---|---|---|---|---|---|---|

| Wireline | Voice | Local and access | 615.1 | 598.9 | 570.5 | 564.7 | 586.9 | 3.9 | -1.2 |

| Long-distance | 457.9 | 406.8 | 300.2 | 339.0 | 348.4 | 2.8 | -6.6 | ||

| Subtotal | 1,073.0 | 1,005.6 | 870.8 | 903.7 | 935.3 | 3.5 | -3.4 | ||

| Non-voice | Internet | 588.8 | 557.6 | 571.4 | 674.1 | 751.5 | 11.5 | 6.3 | |

| Data | 600.0 | 633.7 | 683.8 | 716.9 | 797.2 | 11.2 | 7.4 | ||

| Private line | 593.2 | 545.7 | 524.9 | 510.6 | 450.0 | -11.9 | -6.7 | ||

| Subtotal | 1,782.1 | 1,737.0 | 1,780.1 | 1,901.5 | 1,998.7 | 5.1 | 2.9 | ||

| All | Wireline | 2,855.1 | 2,742.7 | 2,650.9 | 2,805.2 | 2,934.0 | 4.6 | 0.7 | |

| Mobile | All | Mobile | 1,200.0 | 1,277.1 | 1,193.4 | 1,247.3 | 1,180.8 | -5.3 | -0.4 |

| All | Total | Total | 4,055.1 | 4,019.8 | 3,844.3 | 4,052.5 | 4,114.8 | 1.5 | 0.4 |

Source: CRTC data collection

Wholesale services are services provided by one TSP to another, usually when the latter does not have end-to-end facilities of its own.

In 2020, the wholesale telecommunications sector was worth $4.1 billion, of which 28.7% was for the provision of mobile services and 71.3% for wireline services. From 2016 to 2020, wholesale mobile revenues decreased at an average annual rate of 0.4%, comparable to the little or no change for wholesale wireline revenues (despite fluctuations between 2016 and 2020).

Wholesale voice revenues declined, on average, by 3.4% annually from 2016 to 2020, whereas wireline non-voice revenues increased, on average, by 2.9% annually during the same period.

With 69.9% of wholesale wireline revenues, incumbent TSPs maintained the largest share of the wholesale wireline sector, which has decreased slightly from 70.8% in 2019.

Independent ISPsFootnote 8 frequently depend on access services offered by the incumbent TSPs and the cable-based carriers to connect to their customers. Over the years, sales of cable-based access services, known as third-party Internet access (TPIA) services, to independent ISPs have increased, growing at an annual rate of 10.3% since 2016.

The number of wholesale high-speed Internet access lines and revenues grew in 2020. Ontario had the largest share of wholesale lines (59.4%) and revenues (63.0%) in 2020.

Scroll

View data

Scroll

View data

Information in the above figures regarding high-speed Internet wholesale lines and revenues is from a sample of the larger ISPs. They reported approximately 80% of total wholesale Internet service revenues in 2020.

As mentioned earlier, the number of wholesale Internet lines has exceeded 1.3 million, growing at an annual rate of 4.8% from 2016 to 2020. While the number of wholesale Internet lines with download speeds of 50 Mbps and above have been increasing, the majority of wholesale Internet lines still fall under 50 Mbps (57.4% share or 0.77 million lines).

Wholesale Internet lines with download speeds of a gigabit per second and above saw the largest growth (600.0%), more than seven times the number of wholesale lines from the previous year.

Scroll

View data

Source: CRTC data collection

vi. Datasets available on Open Data

There are four Excel workbooks and CSV zips related to this report that have been published on the Open Data portal. They contain the data found in the figures and tables in this section of the CMR, in addition to supplementary datasets (T-S1 to T-S5, W1 to W18, LLD1 to LLD11 and DPL1 to DPL9) that originate from earlier editions of the CMR.

Instructions: Use the table below to search for datasets available on Open Data that are related to this section of the CMR. When you have found the dataset, go to the Find a CMR Dataset page and download the workbooks Data - Telecommunications sector, Data - Wholesale (telecommunications), Data - Local and long distance, and Data - Data and private line. Search for the ‘tab name’ in the Excel workbook tabs to locate the data.

| Workbook | Tab name | Title |

|---|---|---|

| Data - Telecommunications sector | T-I1 | Overview of total telecommunications revenues |

| Data - Telecommunications sector | T-I2 | Telecom revenue share by sector (%) |

| Data - Telecommunications sector | T-I3 | Overview of retail vs wholesale revenue share (%) |

| Data - Telecommunications sector | T-I4 | Overview of key indicators of telecommunications financial performance |

| Data - Telecommunications sector | T-I5 | Overview of retail revenues by sector |

| Data - Telecommunications sector | T-I6 | Highlights of mobile coverage |

| Data - Telecommunications sector | T-I7 | Overview of retail fixed Internet sector |

| Data - Telecommunications sector | T-F1 | Gross domestic product (GDP) growth rate (%) in Canada |

| Data - Telecommunications sector | T-F2 | Total telecommunications revenues ($ billions) and growth rates (%) |

| Data - Telecommunications sector | T-F3 | Total revenues by type of TSP ($ billions) |

| Data - Telecommunications sector | T-F4 | Companies providing telecommunications services by type of TSP (%) |

| Data - Telecommunications sector | T-F5 | Distribution of TSPs by the number of sectors with services offered (%) |

| Data - Telecommunications sector | T-F6 | TSPs’ revenue share grouped by the number of sectors with services offered (%) |

| Data - Telecommunications sector | T-F7 | Telecommunications revenues by category and province/territory ($ millions) |

| Data - Telecommunications sector | T-F8 | Wholesale high-speed access enabled lines by region (thousands) |

| Data - Telecommunications sector | T-F9 | Subsidy paid to incumbent local exchange carriers ($ millions) and contribution rate (%) |

| Data - Telecommunications sector | T-F10 | Telecommunications capital expenditures by type ($ billions) |

| Data - Telecommunications sector | T-F11 | Capital intensity for industries with the highest capital intensity ratios (%) |

| Data - Telecommunications sector | T-F12 | Telecommunications capital intensity (%), by type of TSP |

| Data - Telecommunications sector | T-F13 | EBITDA margins by sector (%) |

| Data - Telecommunications sector | T-F14 | Retail mobile revenue market share (%) |

| Data - Telecommunications sector | T-F15 | Percentage of high-speed Internet wholesale lines by region (%) |

| Data - Telecommunications sector | T-F16 | Percentage of high-speed Internet wholesale revenues share by region (%) |

| Data - Telecommunications sector | T-F17 | Wholesale high-speed access enabled lines by download speed (thousands) |

| Data - Telecommunications sector | T-T1 | Total revenue market share (%) by type of service provider |

| Data - Telecommunications sector | T-T2 | Percentage of telecommunications revenues generated by forborne services (%) |

| Data - Telecommunications sector | T-T3 | Overview of retail mobile sector |

| Data - Telecommunications sector | T-T4 | Retail mobile and paging service revenue components ($ millions) |

| Data - Telecommunications sector | T-T5 | Retail Internet service revenues ($ millions) |

| Data - Telecommunications sector | T-T6 | Overview of retail fixed wireline voice sector |

| Data - Telecommunications sector | T-T7 | Local and long distance retail revenues ($ millions) |

| Data - Telecommunications sector | T-T8 | Overview of retail data and private line sector |

| Data - Telecommunications sector | T-T9 | Data and private line retail revenues ($ millions) |

| Data - Telecommunications sector | T-T10 | Overview of wholesale market |

| Data - Telecommunications sector | T-T11 | Wholesale telecommunications revenues by sector ($ millions) |

| Data - Telecommunications sector | T-S1 | Telecommunications revenue distribution by region ($ billions) |

| Data - Telecommunications sector | T-S2 | Percentage of retail telecommunications revenues generated by forborne services (%) |

| Data - Telecommunications sector | T-S3 | Telecommunications investments made in plant and equipment, by type of provider of telecommunications service ($ billions) |

| Data - Telecommunications sector | T-S4 | Total 9-1-1 service revenues ($ millions) |

| Data - Telecommunications sector | T-S5 | Wireline retail telecommunications revenue market share (%) by type of service provider |

| Data - Wholesale (telecommunications) | W1 | Wholesale telecommunications revenues by market sector ($ millions) |

| Data - Wholesale (telecommunications) | W2 | Local wholesale telecommunications revenues, by major component ($ millions) |

| Data - Wholesale (telecommunications) | W3 | Local wholesale telecommunications revenues, by province ($ millions) |

| Data - Wholesale (telecommunications) | W4 | Wholesale high-speed access (HSA) based subscriptions across Canada, in percentage of total subscriptions |

| Data - Wholesale (telecommunications) | W5 | Internet-related wholesale revenues by type of service ($ millions) |

| Data - Wholesale (telecommunications) | W6 | Wholesale HSA revenues by service component ($ millions) |

| Data - Wholesale (telecommunications) | W7 | DSL and cable wholesale HSA service subscriptions by type of service (thousands) |

| Data - Wholesale (telecommunications) | W8 | DSL and cable wholesale HSA monthly revenue per enabled subscription ($) |

| Data - Wholesale (telecommunications) | W9 | Wholesale HSA-enabled subscriptions by service speed in Mbps (thousands) |

| Data - Wholesale (telecommunications) | W10 | Data protocol wholesale revenues, by service category ($ millions) |

| Data - Wholesale (telecommunications) | W11 | Wholesale mobile wireless revenues, by type of service ($ millions) |

| Data - Wholesale (telecommunications) | W12 | Local and access lines, by type of TSP (thousands) |

| Data - Wholesale (telecommunications) | W13 | Wireline wholesale telecommunications revenue market share, by type of TSP (%) |

| Data - Wholesale (telecommunications) | W14 | Wholesale local and access revenues, by type of TSP ($ millions) |

| Data - Wholesale (telecommunications) | W15 | Wholesale long distance revenues by type of TSP ($ millions) |

| Data - Wholesale (telecommunications) | W16 | Percentage of wholesale telecommunications revenues generated by forborne services (%) |

| Data - Wholesale (telecommunications) | W17 | Wholesale wireline telecommunications service revenues by type of service (%) |

| Data - Wholesale (telecommunications) | W18 | Inter-provider expenses per revenue dollar for wireline services ($) |

| Data - Local and long distance | LLD1 | Residential local telephone and long distance service revenues by type of TSP ($ millions) |

| Data - Local and long distance | LLD2 | Business local telephone and long distance revenues by type of TSP ($ millions) |

| Data - Local and long distance | LLD3 | Number of retail managed and non-managed local telephone lines (thousands) |

| Data - Local and long distance | LLD4 | Residential and business local telephone lines by type of TSP (thousands) |

| Data - Local and long distance | LLD5 | Residential and business, local and long distance monthly revenues ($), per line |

| Data - Local and long distance | LLD6 | Local telephone retail service monthly revenues ($) per line, by type of TSP |

| Data - Local and long distance | LLD7 | Large incumbent TSPs’ retail long distance revenue market share (%), by region |

| Data - Local and long distance | LLD8 | Large incumbent TSPs' payphone revenues |

| Data - Local and long distance | LLD9 | Large incumbent TSPs' payphone quantities |

| Data - Local and long distance | LLD10 | Retail VoIP local lines, access-dependent and access-independent, by market (millions) |

| Data - Local and long distance | LLD11 | Long distance residential and business monthly revenues ($), per line |

| Data - Data and private line | DPL1 | Retail data service revenues by classification of data protocol used ($ millions) |

| Data - Data and private line | DPL2 | Breakdown of newer data service revenues, by protocol used (%) |

| Data - Data and private line | DPL3 | Private line retail revenues by type of service provider ($ millions) |

| Data - Data and private line | DPL4 | Retail data and private line revenue market share (%), by type of TSP |

| Data - Data and private line | DPL5 | Retail data service revenue market share (%), by type of TSP |

| Data - Data and private line | DPL6 | Retail data service revenue market share (%), by type of service provider and classification of data protocol used |

| Data - Data and private line | DPL7 | Retail private line revenue market share (%) |

| Data - Data and private line | DPL8 | Forborne private line routes |

| Data - Data and private line | DPL9 | Forborne data and private line revenues (%) |

vii. Methodology

Capital expenditures and capital intensity

Capital expenditures (CAPEX) are the costs associated with procuring, constructing, and installing new assets of telecommunications networks, to replace or add to existing assets, or to lease to others. The capital expenditures metric in this report includes data only from companies which supplied both telecom revenue and capital expenditure data.

Capital intensity is the ratio of capital expenditures to revenues. The capital intensity metric of the telecommunications industry found in this report was derived by dividing the total annual capital expenditures by the annual telecommunications revenues of companies that reported capital expenditures. The capital intensity of the Top 5 TSPs was calculated by dividing the sum of their capital expenditures of the Top 5 TSPs by the year-end telecommunications revenues of these TSPs. These TSPs accounted for 90.5% of all capital expenditures in 2020.

The capital intensity for all other industries found in Figure 11 was calculated by dividing the industry CAPEX by the full-year industry revenue. Industry CAPEX and industry revenue can be found in Statistics Canada Tables 34-10-0035-01 and 33-10-0226-01.

Churn rate

The average monthly churn rate is derived by dividing the number of subscribers that have left their service provider in a month by the total number of service subscribers over the same period. The higher the number, the more subscribers are leaving the provider.

Earnings before interest, taxes, depreciation, and amortization

Earnings before interest, taxes, depreciation, and amortization (EBITDA) is the operating revenue after having subtracted operating expenses but before subtracting charges for interest payments, taxes, depreciation, and amortization. The EBITDA margins were determined by dividing the total EBITDA by the total operating revenues. The EBITDA margins were calculated for companies for whom at least 80% of their total revenues are represented by Canadian telecommunications services.

Internet usage: methodology

All information in the residential fixed Internet section regarding usage of gigabytes per month, and subscriptions by advertised speed and advertised download capacity, is from data collected through surveying the larger ISPs. These larger ISPs are assigned forms which report details of the residential Internet access high-speed plans that they provide and offer. These ISPs accounted for approximately 88% of the total number of residential high-speed Internet service subscriptions in 2020.

Assignment of forms/surveys is based on the size of the entity. As such, to reduce regulatory burden, small ISPs are not required to submit this information.

Wholesale Internet lines and revenues by province/territory and region

All information in this section regarding provincial wholesale Internet lines and revenues is from data collected through surveying the larger ISPs. These larger ISPs are telecom providers that have historically provided regulated telecom services (such as WHSA, unbundled loops, and Content Delivery Network [CDN] services). They are assigned forms that report details of their wholesale high-speed Internet access lines and revenues.

These ISPs accounted for approximately 66% of total wholesale Internet revenues in 2020.

Definitions

An alternative service provider is any entity that is not an incumbent TSP. Examples of alternative service providers include Distributel, Rogers, Shaw, TekSavvy, and Vidéotron.

Average revenue per user (ARPU) is a measure of revenue generated per subscriber. This is calculated by dividing the whole-year total revenue by the average number of subscribers from the current and previous year. The number of subscribers is taken from year end data.

Cable-based carriers are former cable monopolies that also provide telecommunications services (e.g. wireline voice, Internet, data and private line, and wireless services). Examples of cable-based carriers include Rogers, Shaw, and Vidéotron.

Average churn rate is a measure of subscriber turnover represented as an average monthly rate.

Earnings before interest, taxes, depreciation and amortization (EBITDA), or Operating Margin is a metric used to measure financial performance. It is expressed as a percentage of total revenues.

The estimated number of households in Canada is calculated by dividing the 4th quarter population estimate for Canada by Statistics Canada by the population to dwelling ratio. In turn, the population to dwelling ratio is calculated by dividing the population of Canada by the number of households found in the Statistics Canada Census 2016.

Facilities-based service providers are any entity that has its own facilities. Examples of facilities‑based service providers include Bell Canada, Rogers, SaskTel, Shaw, TELUS, and Vidéotron.

Fibre-to-the-home (FTTH) refers to fibre optic communication delivery system where fibre extends from a concentrator, remote or central office to a residence.

Fibre-to-the-premises (FTTP) is the equivalent of FTTH but refers to fibre extending to a business instead of a residence.

Fixed-Internet services refers to Internet access service via dial-up, DSL, cable, fibre, fixed wireless, satellite, and other technologies such as Wi-Fi where access is provided to a precise and geographically constrained location; Internet transport service; and other non-connectivity Internet-related services such as equipment, web hosting, data centre services, etc.

Fixed wireless service providers are any entity that provides its services over a wireless network that uses either licensed or unlicensed spectrum to provide communications services, where the service is intended to be used in a fixed location. Examples of fixed wireless service providers include SSi Canada and Xplornet.

HSPA, HSPA+, LTE, LTE-Advanced (LTE-A), 5G: High-Speed Packet Access (HSPA) and Long-Term Evolution (LTE) are the protocols or standards used for communications between a mobile phone and cell towers in mobile networks. HSPA is also referred to as 3G (third generation) cellular while LTE is referred to a 4G (fourth generation) cellular. HSPA+, or evolved High-Speed Packet Access, is a form of HSPA that uses technical measures to provide faster transmission speeds. LTE is the current standard that is now widely deployed in most mobile networks, while LTE-Advanced (LTE-A) is an enhancement of the LTE standard. 5G (NR) New Radio is a new radio access technology (RAT) that is referred to as the fifth generation. These networks promise to deliver significantly faster speeds, lower latency, and gains in spectral efficiency than prior generational networks, among other benefits

Incumbent local exchange carrier (ILECs) are incumbent entities providing local voice services. Examples of incumbent local exchange carriers include Bell Canada, Execulink, SaskTel, Sogetel, and TELUS.

An Incumbent Telecommunications Service Provider (TSP) is a company that provides local telecommunications services on a monopoly basis prior to the introduction of competition. These can be further categorized as large and small incumbent TSPs.

An independent Internet service provider (ISP) refers to ISPs that are not cable-based carriers or incumbent TSPs. Examples of independent ISPs include Distributel, TekSavvy, Verizon Canada, and Xplornet.

Large incumbent TSPs serve relatively large geographical areas, usually including both rural and urban populations, and provide wireline voice, Internet, data and private line, wireless, and other services. Examples of large incumbent TSPs include Bell, SaskTel and TELUS.

Mobile Phone revenues and subscribers are derived from handheld devices that are used mainly for voice and data communications, such as cellphones and smartphones.

Mobile Broadband revenues and subscribers include built-in and portable access devices such as hubs, dongles, tablets, laptops and netbooks; excluding revenues derived in relation to internet access over mobile phone or handheld devices such as blackberries, iPhone and other smartphones from this category

Other plans for mobile connected devices should include revenues and the number of plans for all other connected peripherals and devices, M2M services (cars, smart meters, trains, consumer electronics/connected ancillary devices) that are not included in or part of the mobile phones and mobile broadband categories.

Other facilities-based carriers refers to providers of telecommunications services that are not incumbent providers but which own and operate telecommunications networks. Examples of other facilities-based carriers include Allstream Business and Xplornet.

Small incumbent TSPs serve relatively small geographical areas. Due to the limited size of their serving areas, these companies do not typically provide facilities-based long distance services. However, they provide a range of wireline voice, Internet, data and private line, and wireless services. Examples of small incumbent TSPs include Execulink and Sogetel.

Tariff services are services whose rates, terms, and conditions are set out in a Commission-approved tariff. Non-tariff services are those telecommunications services whose rates, terms, and conditions are not set out in a Commission-approved tariff. Off-tariff services are those whose prices are filed with the Commission but for which the parties have agreed to an alternate price.

A telecommunications service provider (TSP) refers to any entity providing telecommunications services.

The top three mobile service providers (Top 3), in terms of revenues and subscribers, consists of the Bell Group, Rogers and TELUS. The Bell Group includes Bell Canada, Bell Mobility, Bell MTS, KMTS, Latitude Wireless, NorthernTel Limited Partnership, Northwestel Mobility and Télébec, Limited Partnership. In 2017, MTS Inc.’s figures were included with those of the Bell Group. In 2015, Data & Audio Visual Enterprises Wireless Inc.’s (i.e. Mobilicity, which then became Chatr) figures were included with those of Rogers. From 2013 on, Public Mobile’s figures were included with those of TELUS. Throughout this section, the flanker brands are a subset of the Top 3, unless otherwise stated.

Wholesale-based service providers or non-facilities-based service carriers refers to companies that generally acquire telecommunications services from other providers and either resell those services or create their own network from which to provide services to their customers. A company that owns a small number of facilities but has the vast majority of its operations on leased facilities may also be classified as non-facilities-based. Examples of wholesale-based service providers and non-facilities-based carriers include Distributel and TekSavvy.

A wireless service provider (WSP) is any entity providing wireless services. Examples of wireless service providers include Bell, Rogers, SaskTel, Shaw, TELUS and Vidéotron.

- Date modified: